by Zsolt Darvas and Pia Hüttl

A few days ago the influential IFO Institute published a short paper suggesting that a Greek default inside the euro-area would cost Germany €77.1 billion, while a default combined with an exit from the euro would cost €75.8 billion. The two numbers are about the same, yet unsurprisingly, media reports emphasised that a Grexit would be cheaper for Germany by €1.3 billion (see e.g. a Focus report here).

We think that the publication of such numbers falsely suggests that direct losses can be calculated precisely. Even more importantly, we noticed that the calculation did not consider three major factors:

- the different haircuts likely under the two scenarios,

- private claims,

- other second round losses.

All three factors suggest that direct losses for Germany would be much larger if Greece was to exit the euro.

Before assessing the details of the calculations, let us make our view clear: we think that a Greek default and exit are neither likely nor necessary. It is definitely in the interests of both Greece and its euro-area partners to find a comprehensive agreement that would avoid default and exit, which would make everyone much worse-off. Greece would enter another deep recession, which would push unemployment up further and reduce budget revenues, necessitating another round of harsh fiscal consolidation. Euro-area creditors would lose a lot on their Greek claims and private claims on Greece would also suffer.

The new depreciating Greek drachma may not revive the Greek economy that much (see on this Guntram Wolff’s recent post here and our 2011 post here). Furthermore, a Grexit would have many broader implications beyond economic issues. What are the prospects for a comprehensive agreement?

- Concerning Greek debt sustainability, there are relatively painless options, as we recently argued.

- Agreement on fiscal policy may not be that difficult either. Greece has suffered a lot in the past few years and has implemented major fiscal adjustments. Although the outlook is not too bright, by now the trough in economic activity has perhaps been reached and some economic growth is expected. This should help fiscal accounts and it is likely that no more fiscal adjustment will be necessary. In fact, the EU Commission expects that the cyclical adjusted primary budget surplus of Greece will decline from 8% of GDP in 2014 by about 1 percentage point in both 2015-16, suggesting a fiscal easing: exactly what Greek opposition parties demand. In other words, the new Greek government will be able to reap the benefits of the adjustments made in the past few years.

- The most difficult step may be to secure an agreement on structural policies, because many of the current plans of the Greek opposition parties are in diametrical opposition to reforms agreed under the financial assistance programme. But a compromise has to be found: both sides have strong incentives to agree and structural reforms have to be part of the comprehensive agreement.

While there are very strong incentives to cooperate and therefore a Grexit is not very likely, for the sake of intellectual exchange, we thought it useful to comment on the IFO calculations assessing the impact of default.

The IFO Institute’s calculations considered the German share of the official assistance to Greece (bilateral German loans, Germany’s share in the EFSF and IMF loans) and various European Central Bank claims. They summed-up all of these claims, assuming that all will be written off in the case of a default. While we have some questions considering central bank related claims (which explains the €1.3 billion difference in IFO’s results), there are three more important issues.

The first major problem with these calculations is that they consider the complete write-off of official claims on Greece in both cases. We doubt that this will be the case: there have been many debt restructurings in recent decades, but claims have never been written off completely. See for example, Juan Cruces and Christoph Trebesch's dataset –, which summarises 187 distressed sovereign debt restructurings from 1970-2013.

The average haircut was 38 percent. Moreover, among the two scenarios (default inside versus exit), the haircut would most likely be much higher if Greece was to exit the euro area, since the new Greek drachma would likely depreciate substantially and Greek GDP would contract substantially, thereby reducing

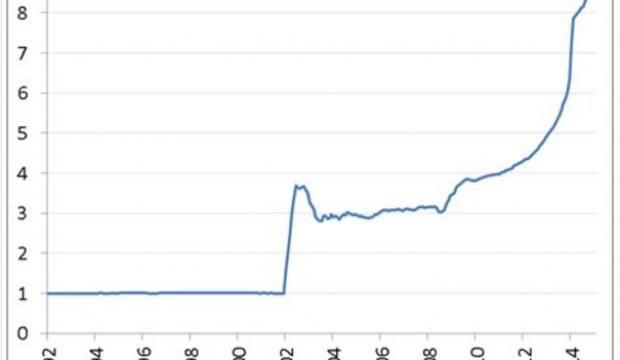

Greece’s ability to honour debts, especially those that are denominated in foreign currencies (in this case, the euro would be a foreign currency). The depreciation of the exchange rate of the Argentine peso in 2002 may be indicative of a hypothetical nominal currency depreciation of the new Greek drachma in the case of a Grexit (Figure 1).

Source: datastream

Second, the the IFO Institute’s calculations do not consider claims by the private sector (though the IFO paper acknowledges this omission). Again, a Grexit would likely lead to much larger losses for the German private sector than a Greek default inside the euro area, since more Greek banks and non-banks would default on the back of a likely massive depreciation of the new currency and contraction of Greek GDP. The table below shows that while German private sector claims on Greece have been reduced substantially since 2009, they still amount to about €16 billion of debt-type claims (the sum of portfolio debt and banking exposure) and about €3 billion of equity-type claims (the sum of FDI ad portfolio equity).